With two young kids in tow, I started to worry about what would happen to them if Mr. LJ and/or I should die tomorrow.

It sounds crass and ominous. But as a parent, I feel a strong responsibility to our two kids. My fear is that if we “dropped dead tomorrow” that they are left in destitute or at the whims of government support programs.

We already did our wills after the birth of our first child, so we took care of the legal technicalities of who would manage our financial affairs or who would be the child(ren)’s legal guardians.

But with a second child, I wasn’t sure there would be enough money to take care of them adequately. It was time to relook at our existing coverage amounts and calculate whether it still met our needs.

Our existing $1M life insurance policy covered our mortgage

When we first married and purchased our house, Mr. LJ and I each purchased a term life insurance policy. At the time, we were in our mid-30s and didn’t have any kids. If one spouse passed away, the only financial obligation for the surviving spouse was the house mortgage.

Since our 30-year mortgage had $800,000 outstanding, we each took a $1M term life insurance policy to age 65. Any extra money beyond the mortgage can provide a few years of relief from full-time work for the surviving spouse. After that, the survivor would need to continue working to make enough to pay for ongoing living expenses without the largest household expense: mortgage payments.

We ignored our employer-funded, minor life insurance policies

The main reason is that Mr. LJ or I can change employers and our life insurance coverage could change or disappear entirely. Instead of relying on employer benefits for coverage, I have just considered these payouts as “cherry on top” in the future.

For reference, my employer funds a laughably small insurance payout of $25,000. Mr. LJ’s coverage is better at $120,000. Neither are sufficient to support two young children’s living expenses until adulthood.

What areas did we want insurance coverage for?

To figure out how much dollar coverage we needed, we needed to understand what areas we needed coverage for. So, Mr. LJ and I discussed what we want out of life if one of us died tomorrow.

- Would we stay in our current house? Yes, we didn’t want to figure out moving to a new home with 2 kids.

- Would we want to work a full-time job or be a stay-at-home single parent? We wanted enough funds to have the option of staying at home to support the 2 kids until they finished high school.

- Would we want to keep the same standard of living or increase/decrease it? We’re simple and don’t have any extravagant wants. Keeping to the same standard of living works.

Based on what life would look like as a single parent that stays at home with no income, I listed out the areas that required financial protection:

- Mortgage balance outstanding: the surviving spouse should not be burdened with recurring, hefty mortgage payments

- “Kids fund”: the kids should each have money set aside for their post-secondary tuition or a “piggy bank” for other future expenses

- Income replacement: using our current annual expenses (excluding recurring savings), the surviving spouse would have enough funds in today’s dollars to not work again until the youngest kid is 18 years old

- Retirement funds: the surviving spouse would have enough funds in today’s dollars set aside for retirement in 20 years

With that, we can calculate the dollar coverage required for each of the 4 areas to figure out total coverage needs.

How much dollar coverage do we need?

Our biggest financial risk occurs if one of us dropped dead tomorrow. With each passing month, our financial requirements decrease, as we are presumably saving more money over time and reducing the time until the kids reach adulthood.

To calculate the maximum dollar coverage we need, the assumption is one of us dies tomorrow and the life insurance is paid out shortly thereafter. This means we need to calculate the dollar requirement for each of the 4 areas in terms of today’s dollars.

Mortgage: this is the most straight forward one to determine coverage. We used our current outstanding mortgage balance as of today, which was $640,000.

Kids fund: post-secondary tuition and ancillary costs varies a lot. Will the kids live at home or on residence? Will they enroll in a specialized programs with high tuition costs? Using my own alma mater (University of Waterloo), annual tuition costs are $9,000 to $18,000 as of 2024/2025. Annual living expenses are estimated at $19,000 to $24,000. In total, a 4 year degree would cost a whopping $112,000 to $168,000!

We have roughly $15,000 of RESPs for each child already saved. Using the low end estimate of $112,000 and deducting the RESPs, we would need ~$100,000 of coverage per child in today’s dollars, or $200,000 coverage altogether. We figured if the kids needed more money for school, they would be eligible for OSAP loans or can contribute with summer/co-op jobs.

Income replacement: excluding mortgage payments and savings, we currently spend ~$100,000 annually. Sure, it’s possible that spending decreases with one less adult in the household, but it’d be offset by more children’s expenses as they grow older (sports, after school classes, etc.)

While it may seem we need $1.8M of coverage ($100,000 for 18 years), we don’t need a full $1.8M tomorrow. Instead, we need the present value of an 18-year annuity for $100,000. Using 4% real returns as a discount rate, the present value would be $1.3M.

Retirement funding: Assuming the same $100,000 spending is needed in retirement, a 4% withdrawal rate would mean a $2.5M retirement portfolio is required at retirement in 20 years.

The present value of a $2.5M portfolio in 20 years is equivalent to $1.2M today (assuming 4% real returns). With $1,000,000 in our current retirement portfolio, it means we need $230,000 insurance coverage today.

| Type | Amount Required |

| Mortgage | $640,000 |

| Kids Fund | $200,000 |

| Income Replacement | $1,300,000 |

| Retirement Funding | $230,000 |

| Total Insurance Required | $2,370,000 |

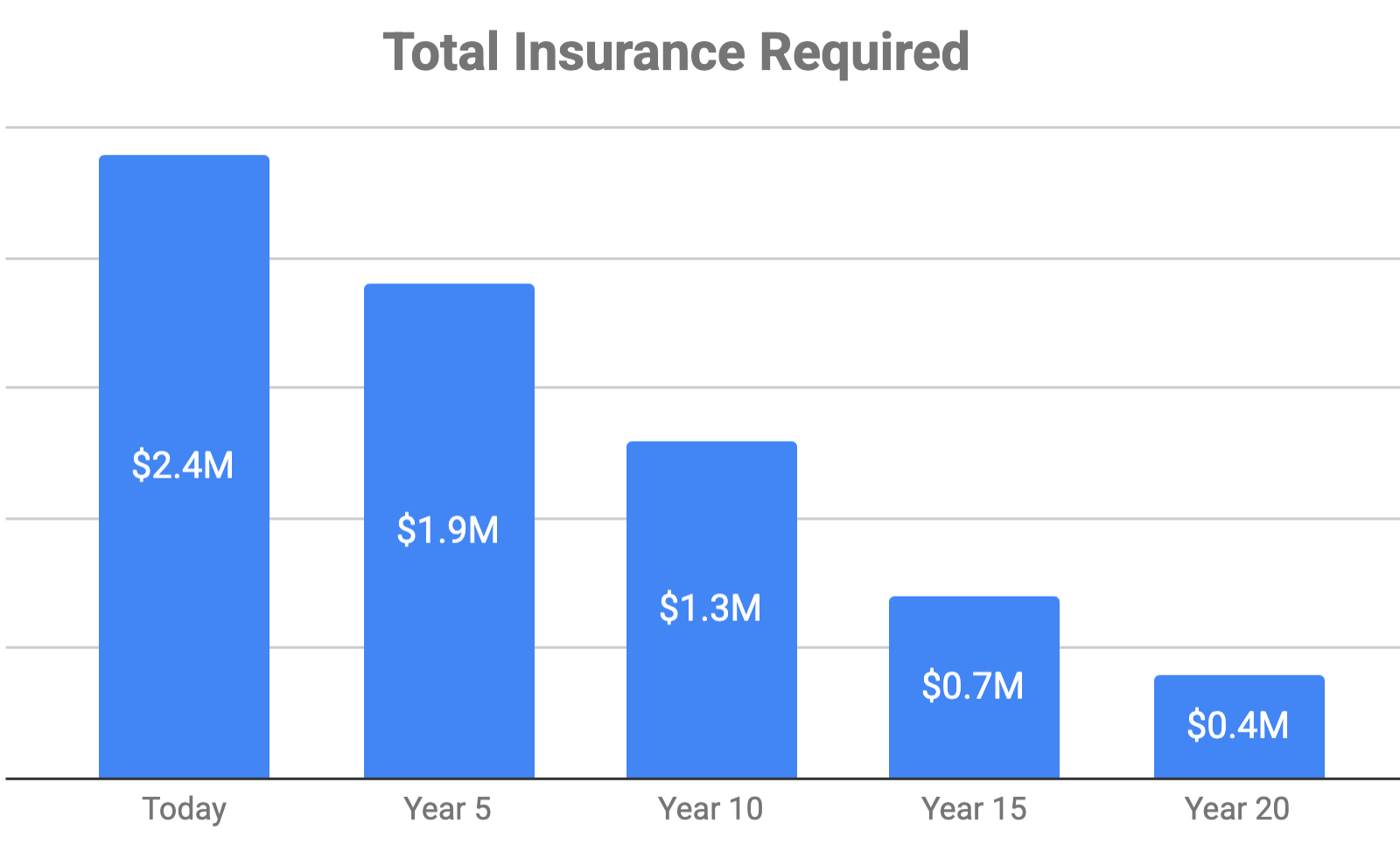

We would need $2.4M of insurance coverage today

Of course, $2.4M is the amount if one of us died tomorrow. As time passes, the amount of insurance coverage require would reduce. It wouldn’t make sense to hold a constant $2.4M worth of insurance policies for the next 20 years!

I projected what the total insurance required is for each of the next 20 years. As example, as each year passes, the “Income Replacement” amount decreases as it’s one less year to support ongoing expenses.

Based on the total insurance required dropping in this manner, I considered stacking two insurance policies with two different terms to save on costs.

| Policy | Today | Year 5 | Year 10 | Year 15 | Year 20 |

| Existing | $1.0M | $1.0M | $1.0M | $1.0M | $1.0M |

| Term 10 | $0.5M | $0.5M | $0.5M | – | – |

| Term 15 | $0.5M | $0.5M | $0.5M | $0.5M | – |

| Total Coverage | $2.0M | $2.0M | $2.0M | $1.5M | $1.0M |

This would leave us short of our total insurance needs in the first 5 years. For complete coverage, we should add a 5-year policy covering $0.5 million. However, I think the concern is low – we have been very conservative in ignoring some employer policies and the ability to tighten the budgets over 15-20 years to make the numbers work.

When I received quotes on stacking insurance policies, it was just a negligible cost savings versus just a 15-year term at $1.0M coverage. It was just saving $10 per person per year! Given the negligible cost, it was not worth setting up two separate policies.

We were just about to proceed with each spouse adding a $1.0M 15-year term policies. Instead, our broker suggested extending the $1.0M policy to a 20-year term for a slightly higher cost of $100 per person per year. If we find that we don’t need to carry the $1.0M policy anymore by year 15, we can simply drop the policy but the extended term gives us some flexibility in case our projections are proven incorrect.

In the end, we each bought a $1.0M policy to span the next 20 years.

Kids change everything, including insurance coverage

In the best case scenario, I hope that we never have to receive any life insurance payouts. But life is unpredictable and kids require a lot. Even if one (or both) of us parents should pass, the best position I can leave them is to have sufficient financial support to take them into adulthood.